Deal or No Deal: Valuing A 6 Unit Multi-Family

Deal or No Deal: An ongoing series where I value a specific property. This property is an 6 unit apartment building listed for $1,600,000.

A regular feature I do is called “Deal or No Deal”, where I find a random property on the internet (oh, excuse me, web 3.0) and go through my proprietary (lol) underwriting process to determine if it is worth buying.

In previous articles here and here, I outlined my 3 step process for evaluating a property:

Does this generally meet my screening criteria? Yes, go to 2.

Does this pass back of the napkin math? Yes, go to 3.

Perform underwriting.

Today’s article is a property submitted from Colin (@heythecolin), the proud owner of a 2003 Ford Focus. Since this is an acquisition Colin is in the process of pursuing, I will be leaving out any identifying information.

Spoiler alert for today’s property: Property tax increase strikes again!

Property: 6 Unit Multi-Family Building

Source: Reader submission

Address: Confidential

Units: 6

Asking Price: $1,600,000

Step 1: Does this generally meet my screening criteria?

Yes, so I will go to step 2. (Typically the properties I will evaluate for these articles don’t meet my personal criteria that I listed in this article, but maybe they will meet yours.)

Step 2: What is the back of the napkin math?

Information I need:

Unit breakdown

• 1 bedroom = 6

Market rents (Provided by submitter)

• 1 bedroom = $2,000/month

Market cap rate (Provided by submitter)

• 6.0%

Napkin math:

Gross potential rent (GPR): $2,000/month/unit x 6 units x 12 months = $144,000 annual GPR

Potential actual rent (6% vacancy/credit loss assumption): $144,000 x 94% = $135,360

Potential NOI:

• 30% expense ratio: $135,360 x 70% = $94,752

• 40% expense ratio: $135,360 x 60% = $81,216

Estimated value range

• High: $94,752 NOI / 6.0% market cap rate = $1,579,200

• Low: $81,216 NOI / 6.0% market cap rate = $1,353,600

Selling list price: $1,600,000

• The list price is just above my high value range, so I’m not feeling great about this one, but the property looks to be in very good condition, so let’s continue on to full underwriting.

Step 3: Determine offer price based on full underwriting

If this was a deal I was actually pursuing, I would call the listing broker and possibly set up a property visit to assess the general condition. For the purposes of this article, I will use the broker OM and general assumptions of condition based on the age and property class.

The underwriting model I use is the Apartment Acquisition Model with Monte Carlo Simulation from A.CRE. I will estimate property value using two scenarios:

Property value with in-place financials

Property value with year 2 or so financials I believe are realistic

Scenario 1: Value with in-place financials

1. Determine adjusted NOI from in-place financials

From the broker OM, the following are the in-place expenses:

Taxes: $16,804

Insurance: $3,537

Electric: $2,000

Water: $817

Trash: $1,006

Management: $6,515

Janitorial: $1,500

Repairs & Maintenance: $3,000

Income: The OM P&L shows a 3% vacancy rate. While this is probably true in today’s market, this is too low to underwrite to. I always default to 6%. Perhaps 6% is too conservative for this market, but with only 6 units, a 6% vacancy (and don’t foget credit loss!) isn’t that hard to get to if you have a lot of turnover or one unit goes vacant for a decent amount of time for whatever reason - eviction, crappy property manager, etc. I will use $134,340 gross rent to reflect in-place rents and apply a 6% vacancy/credit loss rate.

Marketing: There is no in-place marketing expense. Since this is located in a metro area, I will use $300 and try to find better tenants through paid advertising rather than free websites.

Administration: There is no in-place administrative expense. These are things like tax returns, your asset management time, etc. I would assume $2,000 for this expense.

Utilities: I will use actual per the OM of $2,817 plus 3% for inflation, as the property is currently 100% occupied.

Payroll: A small property like this requires no payroll.

Repairs & Maintenance: The in-place R&M of $3,000 seems very low (2% of gross rents), even given this property is in pretty good shape (down to studs rehab in 2011). I will assume an R&M expense of about 6% for $8,000.

Management Fee: The seller shows 5%, but this seems low for such a small property. I would normally expect a 3rd party management fee to be 6-8% of collected rent for a property like this. I’ll split the difference and assume 7%.

Property Insurance: Current property insurance is $590/unit, which seems fairly reasonable, so I will use the in-place cost of $3,537. Normally you would want to receive a quote from an insurance agent at this stage.

Property Tax: Per the assessor’s office, the current assessment is only $75,164. Say what?

After doing some digging, the municipality has a stupid method to assign value - this is my shocked face. On the other hand, they had a nice chart explaining how to calculate the assessment. I don’t want to give details on the assessment method as it will probably give away the location to anyone familiar with this municipality.

Based on the equation and using current millage rate, I estimate my property tax will be $35,000, a 2.1x increase over the current owner. Zoinks!

Property tax increases can be a huge trap for a new buyer. Do your homework on what your assessed value will be in the future.

This is what my year 1 operating expenses look like after making these adjustments:

Looking at my total expenses, my estimated OpEx ratio is 50%. Whoa. This is very high as typical is 30-40%. My spidey sense is starting to tingle that we’re probably pushing a rope on this deal.

Adjusted NOI = $126,280 revenue less vacancy - $60,578 adjusted expenses = $65,702

Estimated value = $65,702 NOI / 6.0% market cap rate = $1,095,503

I am significantly lower than the asking price of $1,600,000. I would normally stop here and move on, but since I’m doing an article for a reader, I will continue on for the sake of completeness.

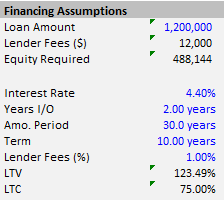

2. Determine Annual Debt Service

This property is a prime candidate for agency debt from either Fannie Mae or Freddie Mac Small Balance Loan programs. If you are an inexperienced buyer, you likely won’t qualify for agency debt without finding an experience partner.

Using the below loan assumptions for lending, my annual debt service will be $74,615.

3. Determine Day 1 CapEx & Annual CapEx Spend

Day 1 CapEx

Reviewing the images in the OM, the property looks to be well maintained. The property was gut rehabbed in 2011, so all the major systems and building structure should be good to go.

The interiors look very good from photos and don’t appear to need any capex. This property looks like the definition of turnkey and there isn’t any obvious day one capex needed, except for potentially 6 hot water heaters that are 10 years old. I will assume $9,000 for 6 new hot water heaters as the only day 1 capex needed.

Estimated Annual CapEx

I estimate annual capex spend with a spreadsheet that captures my entire holding period (10 years) and inflation estimate. If the remaining life of a capex item is longer than my hold period, I do not need to account for this item in my annual capex spend estimate - my spreadsheet will automatically put these as $0.

Pro Tip: Figure out what you need to put into capex reserves on a monthly basis to cover future capex expenses and have the discipline to deposit in a reserve account on a monthly basis.

I’m assuming a 10 year hold period and this property was gut rehabbed 10 years ago, so there is probably limited annual capex needed on the big ticket items, but there is still a decent amount of capex that needs to be planned for - that is the down side to holding properties longer than only 3-5 years like many do.

After filling in all the capex items based on my estimate of life remaining, it looks like this:

Because estimating capex is not a perfect science, I will take the average capex based on my hold period. For this property it is $64/month/unit, which is the unit of measure my model requires as an input.

This equates to $768/unit/year. The normal “rule of thumb” is to assume $250-300/unit/year for capex. You can see how off this assumption can be when you consider all possible capex over your hold period, even for a property in great shape like this one.

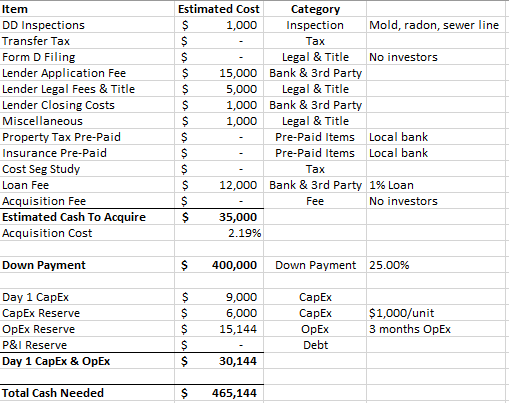

4. Determine total acquisition cost

My estimate for total acquisition cost is $465,144.

5. Determine year 1 cash-on cash return

Annual cash flow = Adjusted NOI - Annual Debt Service - Annual CapEx = $65,702 - $52,800 - $4,608 = $8,294

Total acquisition cost = $465,144

Year 1 Cash-on-cash return = $8,294 / $465,144 = 1.78% (uh oh.)

My normal minimum threshold for year 1 cash-on-cash is 8%, so I’m really far off what I would want for a return.

The boobirds from the cheap seats are saying - “Well, it isn’t a negative cash flow. This is an appreciation play in a major market, bro.”

Au contraire, my speculative friends who gamble on cap rate compression. Remember from the debt service section, I assumed 2 years of interest only (I/O). If I remove the I/O, year 1 cash-on-cash drops to (-)2.31%. Yeah, that’s going to leave a mark.

To meet my 8% minimum cash-on-cash (no I/O) threshold for year 1, the maximum offer I can make is $920,000. I do this by using the “goal seek” function in Excel to fix my desired return at 8% and let Excel find the purchase to give that result.

Even if I’m willing to take a 6% return given this metro area, I’m still at only a $1,015,000 price.

Given I am so far off on the purchase price, I am not going to proceed to scenario 2 of estimating value add potential. The reader indicated markets rents were about 7% higher than in-place and I don’t see that rent growth amount getting this property anywhere close to the seller’s asking price - not that I ever care about the seller’s price as a valuation benchmark, but it is about determining the best use of my time. And there’s no operational expense improvements available to add any significant value.

Closing Thoughts

The property tax increase was a real killer on this property. It’s a tale as old as time. I can’t stress the importance of doing proper diligence on estimating your future taxes.

And the 10 minute napkin math at step 1 worked - hallelujah! The high estimated value was below the asking price, so that was the first sign this probably wasn’t going to work.

The estimated napkin math is always going to skew high as it represents a perfect scenario of all units at market rent, which will never happen. So if the asking price is over the high range, most times you should just move on and save yourself a lot of time.

Good luck to the reader that submitted this as a potential acquisition. Perhaps there is something he knows about the property that I don’t to come up with a higher value - maybe I’m way over-estimating repairs and capex since the building does appear to be in nice shape. I hope that is the case!

Pro Tip: Remember that I’m a simpleton buying properties in very small markets. Do not assume I actually know anything about anything. Caveat emptor with everything you read from everyone on the interwebz.