Deal or No Deal Part 2: Underwriting

A guide for underwriting a multi-family property

In part 1 of Deal or No Deal, I introduced my proprietary (LOL) 3 step process to assess properties:

Does this generally meet my screening criteria? Yes, go to 2.

Does this pass the sniff test a.k.a. back of the napkin math? Yes, go to 3.

Perform underwriting.

Part 1 went through Steps 1 and 2. In this article I will go into detail on Step 3 of underwriting a property for submitting an offer. I focus on multi-family, so any specific numbers I discuss are related to that asset class.

Step 3: Underwriting

Time to complete: 1-2 hours (not including the 147 times you will finagle your assumptions to make the IRR = 15%)

Between Step 2 and 3, I have visited the property to assess the general condition to get an idea of any day 1 capital expenses needed. For a larger property, you likely haven’t gone in every unit at this point, so you’ll still be making some estimates at this stage. And rest assured the selling broker will only show you the nicest units, so assume a bunch of units are a mess and will be needing rehab.

The purpose of Step 3 is to determine your offer price for submitting a non-binding letter of intent (LOI) to the seller. The specific steps needed for underwriting are dependent on your financial model, but the general process is the same regardless of the tool used. I will list all the inputs I use and my general thinking on the general underwriting process.

Model That I Use

I spent probably 50 hours building and tweaking my first Excel model. I don’t suggest you waste your time making your own model. It worked fine for a newbie simpleton such as myself, but I’ve since moved on to using an Excel model from Adventures In Real Estate (A.CRE). I don’t have any affiliation. These guys have forgotten more about real estate than I’ll ever know.

The specific model I use is the Apartment Acquisition Model with Monte Carlo Simulation. I will be writing a future article on Monte Carlo simulation in real estate. For those of you unfamiliar with Monte Carlo, it is a stochastic (random) modeling method that allows for ranges of values in your assumptions vs. fixed assumptions in the typical deterministic modeling that only gives a single outcome.

Pro Tip: If you use someone else’s model, spend time reverse engineering it. You need to understand how the math works.

Underwriting Can Be A Huge Time Suck

Underwriting is where you can waste a tremendous amount of time. Ask me how I know this. Make sure you have done Steps 1 and 2 and subjectively are confident this is a good property before you spend the time to underwrite.

A possible time sink at this step will be from manually putting the seller’s data into a usable format. It’s not uncommon receive files in PDF format, which is not very useful when using Excel.

Pro Tip: Convert tables buried in a PDF to Excel using a free online tool to save yourself a ton of time. Some conversion tools are better than others. Don’t give up if the first one formats the spreadsheet horribly.

The Info Needed To Start

What I need for information at this point:

Current rent roll

Trailing 12 month (T-12) P&L. Sometimes the best you can do at this stage of the process is a prior year P&L. The worst is when all you have is a pro forma in the broker’s OM, which will border on pure fiction.

Estimated lending terms. You should be talking to lenders on a regular basis to have reasonable confidence in these inputs. The “typical” numbers I show below are for non-recourse multi-family loans from national lenders for a small potatoes chump like me. Remember: The bigger the player, the better the loan terms. Local banks will likely not offer these terms.

Rate (3-ish%, depends on term, buyer experience, property, etc.)

Term

Loan-to-Value (LTV) percentage (max 75-80%, depends on property)

Interest only (I/O) period (1-3 years, more for big players)

Amortization period (25-30 years)

Lender fee (1% of loan amount)

Estimate of the total acquisition cost. The following are generally what you need to account for:

Down payment

Inspection costs

Pre-paids: 1 year property tax and insurance

Transfer tax: If any, location dependent

Legal fees: Lender and yours

Title insurance cost

Survey cost

Environmental report cost

Loan application fee: Fannie/Freddie will be about $15,000 - applied toward total lender costs to close

Cost segregation study: Usually makes more sense to do on larger properties as these cost thousands of dollars.

Investor legal docs: If selling a securitized asset i.e. you have investors

SEC and state filings: If selling a securitized asset i.e. you have investors

Acquisition fee: If you have investors and are charging them for your time to find and acquire; typically 1-3% of purchase price. This fee at 3% makes me barf when I see it in an investor deck.

Estimated day 1 capital expense repairs needed: Many times up to 75% of this can be financed by your lender.

Estimated cash reserves at closing for operating expense (OpEx) and capital expense (CapEx) accounts. I typically use 3 months of annual OpEx. For CapEx, I create a detailed estimate of future CapEx needed based on my property visit (discussed later in this article).

Many people will use a ballpark $250 per year per unit for a CapEx reserve amount. Property condition varies wildly, so I’ve never used this rule of thumb at this point of the process. I’ve found the $250 rule of thumb to usually be laughably wrong if you are being honest with yourself about how much CapEx a class C multifamily complex built in 1982 that has neever been fully renovated will need over the next 10 years. Also, if you are making projections, you have to apply inflation to CapEx. I cringe whenever I see a 10 year projection in an investor deck and there is the same CapEx reserve amount for every year.

Underwriting Scenarios To Consider

After compiling all of this information, it is time to start underwriting. I run 2 scenarios:

The property with in-place financials.

The property as I believe I can operate within a year or so down the road. Trying to predict the future much past the first year is a fool’s errand. I will still do this forecasting if investors are involved because investors have been conditioned to see this in a pitch deck. Predicting rent growth, expense growth, vacancy rates, etc. for a 5-10 year period is usually wrong the minute after it is put down on paper, so it’s really an exercise in futility (maybe a little less futile if you are using Monte Carlo simulation).

Scenario 1 of in-place financials tells me what I should pay for the property. My philosophy is that I will not pay a seller for future value that I need to create. It makes no sense to pay a seller for work that I need to do and the risk I will need to take on. Others are willing to pay the current owner for future value, so I may be at a disadvantage with my offer price. But so be it.

Scenario 2 tells me what “forced appreciation” (i.e. NOI increase) I can potentially add through operational efficiencies and/or more aggressive rents. This has nothing to do with predicting future cap rate compression (i.e. speculation).

I put more weight on the Scenario 1 value and the corresponding returns. I am focused on finding day 1 cash flowing properties. As I build my portfolio and have a greater total monthly cash flow, I will be in a better position to try to hit some home runs (i.e. higher risk) through greater value add properties.

Scenario 1: Let’s Get Started

Now to the actual underwriting for Scenario 1:

1. Determine Adjusted NOI From In-Place Financials

This is done by reviewing the seller’s T-12 P&L and making any adjustments that seem very low or high. I don’t usually mess with the in-place revenue for scenario 1 and focus on the expenses as this is where there might be some nonsense you can eliminate, especially if you are buying from a mom and pop seller. Your P&L needs to include these major expense buckets:

Marketing: This can vary depending on the amount of competition in the market. For a small market this could be near $0 by using free online services like Apartments.com, Facebook or Craigslist.

Administrative: Assume 1% of collected revenue to cover your asset management time (plus work you outsource to the Philippines for $0.50/hr).

Utilities: Using actual from the T-12 is usually your best bet at this stage.

Payroll: $0 if you fully outsource. Could be a significant number for on-site staff at larger properties. For larger property payroll, be sure to understand who these people are. Larger properties may be operated by an owner related entity. This can inflate payroll (at the expense of the owner’s investors’ returns).

Repair & Maintenance: Usually in the 5-15% of income range. Will be higher for older properties, lower for newer. Be aware the savvier (scummier) owners may try to bury repairs in their balance sheet as capex to boost NOI, so take the seller’s actual expense with a grain of salt. It’s hard to discover this at the offer stage, but you will likely be able to root it out if you get to contract due diligence.

Property Management: Will be 4-5% of collected revenue for larger properties. About 8% for small properties.

Insurance: Do not assume the current owner’s premium will be your premium. Get a quote from your insurance broker.

Property Tax: Do not assume the current owner’s property tax amount will be your tax amount. Call the tax assessor to understand how they re-assess properties - At time of sale? Based on market price? Are there mandated guidelines on when re-assessments happen? When do they expect to re-assess? What is the expected rate for next year? What has been the rate increase history? Does the locality have plans to spend a ton of money they don’t currently have on infrastructure in the near future?

After making any NOI adjustments, some things you want to sanity check are:

Operating expense ratio: Multi-family will typically have an expense ratio of 30-40%. If the ratio is significantly out of this range either high or low, it is a red flag. Go back to the seller’s P&L and see what their in-place expense ratio is and compare to yours. Being out of range may not be a deal breaker. If the ratio is high, it could indicate potential value to be had through operating improvements. If your ratio is low, double check your numbers to make sure it is real.

Vacancy rate: Does the current vacancy rate makes sense based on your general knowledge of the local market? Generally speaking for today, 5-6% economic vacancy is the typical assumption for vacancy & credit loss, but this is really dependent on the local market. Many areas today are effectively at 0%, but never underwrite to buy at 0%.

Market cap rate: Does the selling price cap rate (Adjusted T-12 NOI / listed selling price) make sense based on your general knowledge of the market? If the calculated cap rate is significantly lower than you expected, it may be worth stopping at this point if you think the seller is not willing to negotiate price significantly.

2. Determine Annual Debt Service

There’s a million different online calculators if your model doesn’t have this built in. If you are going to be underwriting on a frequent basis, build it into your model. Any model you buy will have this capability.

3. Determine Day 1 CapEx Needed & Annual CapEx Spend

This is an extremely important part of your underwriting. CapEx can be enormous and significantly impact the value of a property and its future returns. This is not a step you should gloss over.

Day 1 CapEx: The math to calculate is simple. Just add up all the CapEx items you believe the property needs at day 1 of ownership. If at all possible, have a contractor you trust walk the property with you when you visit the property. As you get more experienced, you can probably do the estimating yourself, certainly on smaller properties, but having a professional opinion on critical deferred maintenance items can be invaluable.

Annual CapEx Spend: This one has a little more complexity to it than Day 1 CapEx as you need to forecast over your hold period the total amount of CapEx you think you will spend annually (and also consider inflation). For the purposes of my valuation calculation, I use the average annual CapEx spend for my hold period.

4. Determine Year 1 Cash-on-Cash Return

This is a simple calculation:

Annual Cash Flow / Total Acquisition Cost x 100 = Cash-on-Cash Return %

Annual Cash Flow = Adjusted NOI - Annual Debt Service - Annual CapEx

For most of the deals I look at, I want a minimum of 8% and target 10%. This is high for large markets, so I don’t bother really looking in thos emarkets. I look at mostly smaller markets, but these returns are unicorns right now even in tiny markets. So I have low expectation that I will close on much at the moment.

So what happens if the Cash-on-Cash return is less than my target? I lower the purchase price I am willing to pay until I meet my target return. Lowering the purchase correspondingly lowers your down payment and reduces the denominator. I would strongly encourage you to not start playing around with the numerator by adjusting income and expenses. You already did that work and should put the NOI number under lock and key at this point (unless you really did make an actual mistake).

Using the market cap rate to determine a property value is fine for a reference point, but I don’t use it as a primary driver to determine value. It’s a very subjective number that can be debated with a seller ad naseum. What cannot be debated is the return I must have to satisfy investors. I get to decide what this is based on my knowledge of their expectations.

Remember: For this Scenario 1, I am determining the value of the property based on adjusted in-place financials and not including any value add opportunities. And I’m not doing any future growth assumptions at this point - if the property doesn’t meet my return target for year 1, it isn’t even worth thinking about year 10. Using IRR, unlevered yield on cost, equity multiple, etc. for this scenario isn’t really helpful in determining value. These metrics will have more use for Scenario 2 where we include potential value add value.

5. Determine Offer Price

Once you have determined your purchase price from step 3 and the Day 1 CapEx from step 4, you can now determine your offer price:

Offer Price = Purchase Price To Achieve Target Cash-on-Cash - Day 1 CapEx

If by some miracle your offer price is even close to the seller price, you may want to buy some lottery tickets to take advantage of your incredible luck.

And that’s it for Scenario 1. Now on to Scenario 2 where we consider any value add opportunities.

Scenario 2: Let’s Get Started

Scenario 2 is where we determine what, if any, value add opportunity there is for this property. As a reminder, value add is where you look to increase the NOI through rent increases and/or expense reduction. This results in increased cash flow and property value.

1. Revisit Scenario 1 Adjusted T-12 NOI

Increasing income will typically be the largest value add opportunity for most properties. Expenses in total are usually only 30-40% of income, so mathematically expenses usually can’t compete with income for adding value.

Rent Increase Value Add: From part 1 of this article series, you already know what the market rent is for this property. Determining if there is any value add from raising rents, you just need to compare the average market rent for the property and the actual average rent. You want to know the annual amount, so the math is

Rent Increase Value Add = (Average Market Rent - Average In-Place Rent) x 12 x Unit Count / Market Cap Rate

Keep in mind this would be the maximum possible value you could add if all units were rented at the market max. In practice, this is not possible as you will always be under market rent for some units - maybe you inherited tenants in older units paying under market and can only bump their rent so much or your plan is to wait for move-outs to rehab and then increase rents (some people will never move).

Pro Tip: Eviction court back-ups due to Covid have made landlord move-out notices at end of lease a bit more risky as there is always a chance a resident won’t move if they didn’t want to, then just stops paying. It may take months for a court date in some instances.

Also, keep in mind that it is only in very rare circumstances will you be able to just simply raise rents without investing some amount of CapEx in unit rehab. You need to consider the ROI of the unit rehab. On a per unit basis, it needs to be accretive to your overall property level return. Otherwise, don’t bother with the rehab.

Expenses: There is no guidebook for determining value add on expenses. A lot of this is based on experience and just taking the time to do your homework well. For example, I recently read a Twitter thread on the value add opportunity for reducing water usage. Much of this knowledge is from having done it before. Operational efficiency is what sets apart the pros from the Joes.

2. Determine Growth Rates

After having created my value add T-12 P&L to determine my value add year 1 NOI, I’m ready to take a look at potential returns over my entire hold period, which I usually estimate at 10 years.

Before I get into 10 year projections, know that I think predicting the future is a fool’s errand. I have no idea what anything in the future will be exactly: rent growth, expense growth, interest rates and on and on. So why do I do it? Two reasons:

Investors have been conditioned to see projections in pitch decks.

I use stochastic (random) modeling that is skewed to be conservative. I’ll never have 100% confidence of being exactly right. This reduces my chances of being 100% exactly wrong. Or it allows me to be wrong 10,000 times instead of just once LOL.

The annual growth assumptions you need to consider for a future projection are:

Rent growth percentage: This amount is market dependent. I typically use 3-3.5%. This assumption is the easiest to juice your returns with. Be honest with yourself on what is realistic. Also, a value add deal that has a lot of unit rehab will require a higher rent growth in early years and lower in later years.

Expense growth percentage: I’ve been using 3-4%, but may start increasing this to account for the high inflation we are seeing. My rule of thumb is I always want to assume a slightly higher expense growth than rent growth for a stabilized year.

Additional income (laundry, storage, etc.) growth percentage: I use 1% as this income is usually small and not a big driver on returns.

Capital expense growth percentage: I usually have this equal to the expense growth.

Cap rate change percentage: I never assume a cap rate compression. I always assume expansion and usually use about 0.10% per year, but it depends on the market. If you see a deal where someone is assuming cap rate compression, this is a red flag.

I only use fixed rate debt with a term as long or longer than my expected hold period, so the interest rate is never an assumption I need to make. If you want to use floating rate or a term shorter than your expected hold period, Godspeed.

3. Review Outputs

Once I dump all these inputs into my model, I then take a look at the deterministic (single value for assumptions) output to see where everything shakes out.

The primary metric I’ve starting using for assessing value add potential is Unlevered Yield On Cost (UYOC).

What Is Unlevered Yield On Cost?

This is a simple calculation that tells you what your returns are before any leverage is included. I like this metric because it tells me if I’m actually buying a good property.

The year 1 UYOC needs to be higher than the going-in cap rate if you are looking at a property that has potential value add (higher risk). Otherwise, what is the point of taking on the value-add risk? How much higher depends on how you are assigning value to the risk of that specific property. Many use a plus 1-2% over cap rate as a ballpark to target.

Unlevered Yield On Cost = NOI / Total Acquisition Cost. This metric removes leverage from returns. Leverage can distort property returns.

For a stabilized property that has fair market in-place rents, the year 1 UYOC will be lower than the going-in cap rate. This makes sense: Remember that the denominator of calculating the cap rate only includes the purchase price (Cap rate = NOI / Purchase price) and does not include all of the costs to acquire.

If the UYOC is higher than the cap rate you assigned for a stabilized property, this is potentially a good deal. It indicates a possibly mispriced asset (aka unicorns in the current market). If UYOC is lower for a stabilized property, it may or may not be a bad thing. It just depends by how much.

Other Metrics To Consider

There’s many other metrics to look at beyond UYOC. I look at cash-on-cash next, because cash flow is of primary importance for my strategy.

In theory for Scenario 2, Year 1 cash-on-cash should be higher than Scenario 1, but it depends on how much value add CapEx was needed. If you are planning a lot of unit rehabs, many rent increases for the full year may not hit until year 2, so year 2 may be the year you want to focus on, not year 1. Year 1 return could actually drop if there will be a lot of units vacant while you rehab.

Pro Tip: If you are a limited partner looking at investing in a heavy value add deal requiring a significant number of units to be taken out of service for rehab in year 1, scrutinize the rent increase to in-place rents shown in year 1 and maybe 2. If they are large, this could be a red flag on poor assumptions.

Assuming I’m happy with the average cash-on-cash for the hold period, I then look at the following:

10 year IRR: Needs to be at least 15% minimum. Target is 20%. I call IRR “Imaginary Rate of Return” because of how easily it can be manipulated.

Equity Multiple: Should be about 3.0 for a 10 year hold. About 2.0 for a 5 year hold.

Year 1 Breakeven Occupancy: Must be less than or equal to 80%.

Price per Unit: I like to sanity check the price per unit vs area single family home prices. If they are similar, it may be a similar cost for a renter to just buy a house.

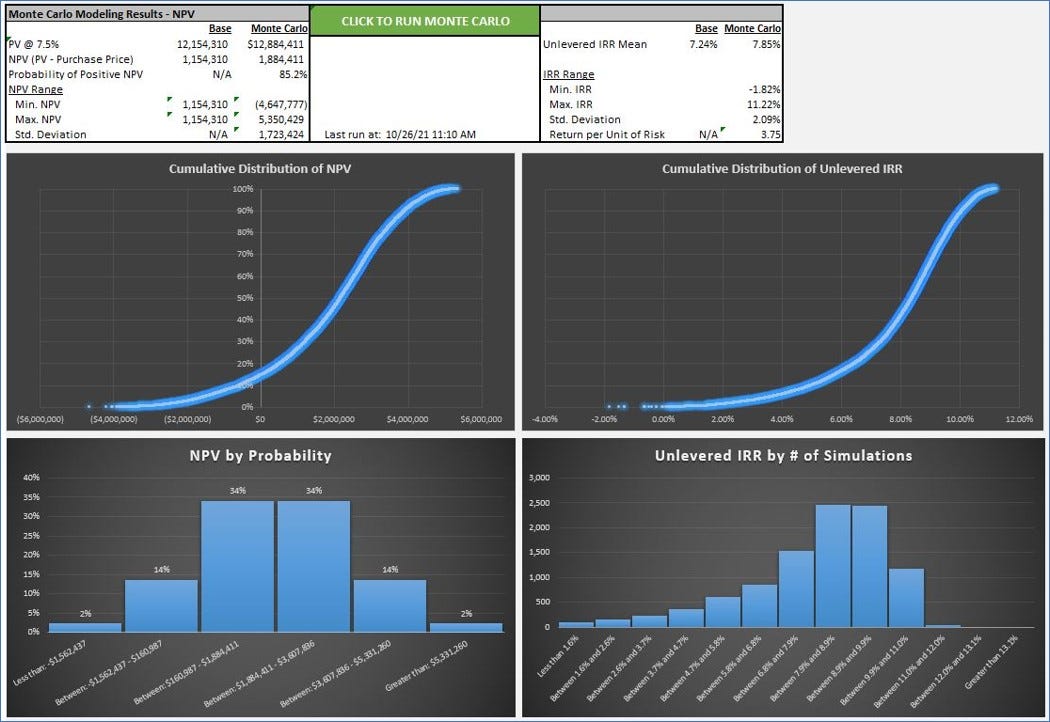

4. Run Random Simulation

The final step I do is determine my inputs for the Monte Carlo simulation. The model I use from A.CRE allows for input ranges for all the major assumptions. I lean towards skewing my ranges on the conservative side. A.CRE has a tutorial on how to use the model. You should have a basic understanding of statistics to use this tool. I got an D in Statistics 101, so you don’t need PhD level expertise. The output looks like the following:

How This Is Useful

It gives me a probability of a positive NPV i.e. the chances I will have theoretically paid less for the property than I should have (a good deal).

It tells me if my single variable assumptions were conservative or aggressive. Many investors will want to just see “one number” for returns since this is how every deal is marketed.

It quantifies a return vs. risk multiple. This can be useful for comparing similar type investments.

It makes pretty charts.

I will be writing a future article on Monte Carlo simulation for real estate. I like random modeling because:

Even though I’m a simpleton, I’m not dumb enough to think I can predict the future exactly. Random modeling doesn’t fix the garbage in, garbage out problem, but it reduces your chances of making really bad assumptions.

I can present a more realistic view of possible outcomes to investors. The typical deterministic models showing a single outcome is silly for anyone who thinks about all the assumptions being made.

And that’s it for how I underwrite. Just 473 paragraphs of clearly written gobbledygook. So simple, even a caveman can do it.

Remember: Garbage in will equal garbage out. You have to know the market you are buying in. You have to have reasonable confidence in operating expenses. You have to have reasonable confidence in capital expenses. If you are a newbie, you are at a disadvantage. But that’s life. Take some small risks to get started and go from there.

If you liked this article, please go to the nearest street corner and tell everyone that passes by to subscribe and to follow me on Twitter because there is no one else talking about real estate on the internet.

Why does this article have so few visits? It's great! Really high quality here.

Do you buy property that is close to you, or anywhere in the US? Also, if you pick something out of state, do you always walk it before pulling the trigger? Or if it is of lower value would you do an online analysis and call it a day?

"thos emarkets" - plz fix