Deal or No Deal: Valuing A 6 Unit Multi-Family

Deal or No Deal: Valuing A 6 Unit Multi-Family

Deal or No Deal: An ongoing regular series where I value a specific property. This property is a 6 unit apartment building in a small Maine city listed for $749,000.

In previous articles here and here, I showed you my 3 step process for evaluating a property:

Does this generally meet my screening criteria? Yes, go to 2.

Does this pass the sniff test a.k.a. back of the napkin math? Yes, go to 3.

Perform underwriting.

The properties I evaluate in these articles will be listed online using publicly posted information that you can access yourself.

Spoiler alert: This property went under contract yesterday after I had already started this article. 5 days on the market. Not surprising after underwriting this property.

Property: 6 Unit Multi-Family Building

Source: NECPE

Address: 29 Cutts St, Biddeford, ME

Units: 6

Asking Price: $749,000

Step 1: Does this generally meet my screening criteria?

Yes, so I will go to step 2. (Typically the properties I will evaluate for these articles don’t meet my personal criteria that I listed in this article, but maybe they will meet yours.)

Step 2: What is the back of the napkin math?

Information I need:

Unit breakdown

• 3 bedroom = 6 (3 currently vacant)

Market rents (Normally I already know market rents for an area, but for these random properties I am evaluating in areas I may not be familiar with, I will be using the fair market rents published by HUD, which are generally pretty accurate for middle of the road type properties.)

• 3 bedroom = $1561/month

Market cap rate

• 7.5%

Napkin math:

Gross potential rent (GPR): $1561/month/unit x 6 units x 12 months = $105,648 annual GPR

Potential actual rent (6% vacancy/credit loss assumption): $105,648 x 94% = $99,309

Potential NOI:

• 30% expense ratio: $99,309 x 70% = $73,954

• 40% expense ratio: $99,309 x 60% = $63,389

Estimated value range

• High: $73,954 NOI / 7.5% market cap rate = $986,052

• Low: $63,389 NOI / 7.5% market cap rate = $845,188

Selling list price: $749,000

• The list price is well below the low end of my value estimate range, so this is a potential good/great deal.

Since this property passes the napkin math test, I will proceed to full underwriting.

Step 3: Determine offer price based on full underwriting

If this was a deal I was actually pursuing, I would call the listing broker and possibly set up a property visit to assess the general condition. For the purposes of this article, I will use the online images and general assumptions of condition based on the age and property class.

The underwriting model I use is the Apartment Acquisition Model with Monte Carlo Simulation from A.CRE. I will estimate property value using two scenarios:

Property value with in-place financials

Property value with year 2 or so financials I believe are realistic

Scenario 1: Value with in-place financials

1. Determine adjusted NOI from in-place financials

From the broker listing, below are the in-place expenses:

Property Tax: $7,104

Insurance: $4,829

Utilities: $6,381

No other expenses were given, so I will have to make assumptions on the remaining items.

2. Make adjustments/additions to in-place financials

Income: The listing did not give a rent roll, but it stated 3 units are vacant and the other 3 are “way below market rate” - OK, I’ve never heard this before from a broker. If market rent is about $1,560, I will assume the occupied units are currently at $1,300.

Current Income = ($1,300/month/unit x 3 units + $0/month/unit x 3 units) x 12 = $46,800

Since it will likely be easy to fill these units as the condition looks pretty good, I will assume the vacant units will rent at market rate of $1,560/month.

Adjusted annual income = $102,960.

Normally, I would not adjust income for the scenario 1 analysis, but 3 vacant units in a 6 unit building in good condition is not normal in this market.

Property Tax: Per the assessor’s office, the current assessment is $389,700. If we were to buy at about $750,000, we can expect our tax to be about 1.9x the current, so I will assume $13,500 for annual taxes. These big tax increases always make me start to get very sweaty.

Normally you would want to call the tax assessor and find out specifically how properties are re-assessed at time of sale. I did not call the tax assessor to verify my 4x increase assumption as I would be wasting their time since I’m not interested in actually buying this property. Property tax increases can be a huge trap for a new buyer. Do your homework on what your assessed value will be in the future.

Property Insurance: Current property insurance is $805/unit. Based on my experience, this is high - definitely high if I were to add this property to my existing master policy. I will use $500/unit, so I will assume $3,000 for insurance. Normally you would want to receive a quote from an insurance agent at this stage.

Utilities: I will use actual per the listing multiplied by 1.75 to account for a fully occupied building, so I will assume $11,000.

Management Fee: There was no expense listed. I would normally expect a 3rd party management fee to be 8% of collected rent for a very small property like this. I will assume $7,743.

Maintenance & Repairs: There was no expense listed. This is a good condition building built in 1900. I will assume about 8% of income for $8,000 annually.

Marketing: In the current rental market for properties like this, there are many free advertising options that work just fine. I will use $100, but this will be inconsequential to the valuation.

Payroll: A small property like this requires no payroll. I will assume $0.

Administration: There was no expense listed. There are things like tax returns, your asset management time, etc. that need to be accounted for in expenses. I would assume $1,000 for this expense.

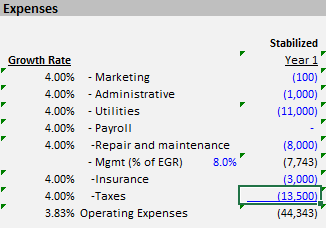

This is what my year 1 operating expenses look like after making these adjustments:

Looking at my total expenses, my estimated OpEx ratio is 43% even with the huge property tax increase the new buyer will incur. The ratio is a bit on the high side as typical is 30-40%, but not too bad for a building where the landlord is supplying heat.

Adjusted NOI = $96,782 revenue less vacancy - $44,343 adjusted expenses = $52,440

Estimated value = $52,440 NOI / 7.5% market cap rate = $699,200

I’m not too far off the asking price, so let’s continue with the analysis.

3. Determine Annual Debt Service

Using the below loan assumptions for lending from a local bank, my annual debt service will be $31,503.

4. Determine Day 1 CapEx & Annual CapEx Spend

Day 1 CapEx

Reviewing the images in the listing and Google satellite and streetview, the property looks to be well maintained. The roof appear to be in good shape, which is usually a huge potential capex expense.

The parking lot looks to be in average condition, but nothing terrible. Regular maintenance appears all that is needed and we’ve captured that in our adjusted repair & maintenance line item.

The interiors are somewhat dated, but look in decent condition. The vacant units appear to be move-in ready, so no capex needed there. Based on the overall condition of the property, I will assume that all units are in generally decent shape and have 80% life left for all interior capex items.

The listing stated the heating system is from 2015, so that should last for our 10 year hold period with regular maintenance.

I can’t see any day 1 capex needed based on the images, but it will never be $0. I will assume I will need $2,000 to cover various day 1 capex.

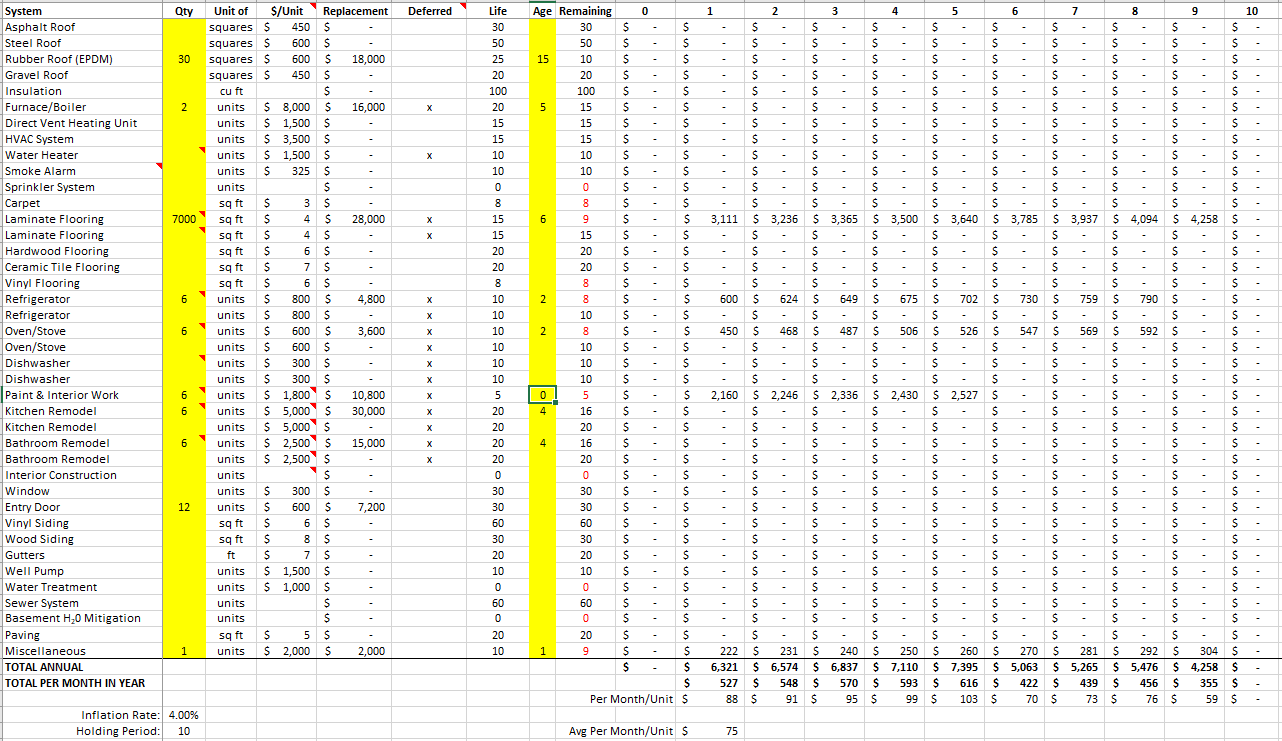

Estimated Annual CapEx

I estimate annual capex spend with a spreadsheet that captures my entire holding period (10 years) and inflation estimate. If the remaining life of a capex item is longer than my hold period, I do not need to account for this item in my annual capex spend estimate - my spreadsheet will automatically put these as $0.

After filling in all the capex items based on my estimate of life remaining, it looks like this:

I am making the assumption that I will be replacing all of the existing carpet and vinyl flooring with laminate flooring as units are turned over. A decent laminate plank floor looks pretty good and is almost indestructible.

Because estimating capex is not a perfect science, I will take the average annual capex based on my hold period. For this property it is $75/month/unit, which is the unit of measure my model requires as an input.

This equates to $900/unit/year. The normal “rule of thumb” is to assume $250/unit/year for capex. You can see how off this assumption can be when you consider all possible capex over your hold period.

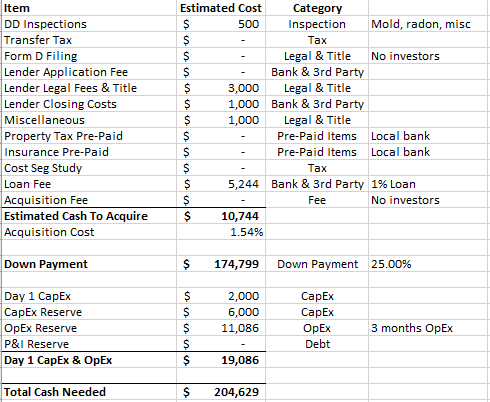

5. Determine total acquisition cost

My estimate for total acquisition cost is $204,629.

6. Determine year 1 cash-on cash return

Annual cash flow = Adjusted NOI - Annual Debt Service - Annual CapEx = $52,440 - $31,503 - $5,616 = $15,321

Total acquisition cost = $204,629

Year 1 Cash-on-cash return = $15,321 / $204,629 = 7.5%

My normal minimum threshold for year 1 cash-on-cash is 8% for a property like this in a small market. I’m close enough at 7.5% because I’m dumb enough to know my estimates to calculate the cash-on-cash return aren’t perfect.

If I were to adjust the purchase price to $749,000, the year 1 cash on cash return drops to 6.1%. This isn’t terrible, but it drops below my typical minimum threshold of 8% for scenario 1. Would I still buy at the list price of $749,000? Maybe, depending on what the scenario 2 upside looks like.

So for scenario 1, I’ve determined I am definitely willing to buy the property at about $700,000 as this will give me an approximate year 1 cash on cash return of 7.5%. Since I’ve met my first hurdle of day 1 cash-on-cash return, I will now proceed to scenario 2 of determining if there is any future value to capture based on further adjusting in-place financials from scenario 1.

Scenario 2: Estimating Value Add Potential

Scenario 2 is where we determine what, if any, value add opportunity there is for this property. As a reminder, value add is where you look to increase the NOI through rent increases and/or expense reductions. This results in increased cash flow and property value.

1. Revisit Scenario 1 Adjusted T-12 NOI

Rent Increase Value Add: We’ve already put 3 units up to market rent in scenario 1 as they are currently vacant. The remaining 3 we assumed have below market rent of $1300/month. Bringing these 3 units to market rent, we can gain:

Rent Increase Cash Flow Add = ($1560/unit/month - $1300/unit/month) x 3 x 12 = $9,360 annual

Rent Increase Value Add = $9,360 / 7.5% cap rate = $124,800

Cost: It’s unknown if any capex is needed to upgrade the 3 occupied units, but this would be a no brainer even if it was $15,000 to rehab the units.

Year 1 ROI = $9,360 / $15,000 = 62%

Expenses Value Add: We already adjusted most of the expenses in scenario 1, so there isn’t much to do here. The only one that might be possible is with utilities.

Many older buildings have not yet been converted to using hybrid hot water heaters. If these are placed in an optimum location (like a warm boiler/furnace room that this building likely has), these will run very inexpensively. The extra bonus is that some states like Maine offer big rebates on hybrid hot water heaters, so they aren’t any more expensive than electric.

By installing two hybrid hot water heaters in the boiler room, I estimate we can reduce heating oil usage by 20% based on previous experience. This also gives the added benefit of increased boiler life as we can shut the boilers down for about 4-5 months of the year.

Oil Cost Savings Cash Flow = $4,523 x 20% = $905 annual savings

Oil Cost Savings Value = $905 annual savings / 7.5% cap rate = $12,067

Cost: $3,000 for 2 hybrid water heaters installed

Year 1 ROI = $905 / $3,000 = 30%

In total, I believe there is about $10,000 in best-case increased cash flow available (on top of in-place cash flow of $15,384 from scenario 1) with a non-recurring cost of $18,000. This will add about $130,000 in property value. Not too shabby.

2. Determine Growth Rates

The annual growth assumptions for the 10 year projection are:

Rent growth percentage: 3% for this small market, which is a typical historic rent inflation amount.

Expense growth percentage: 4%. My rule of thumb is I always want to assume a slightly higher expense growth than rent growth for a stabilized year.

Additional income (laundry, storage, etc.) growth percentage: Property has no additional income.

Capital expense growth percentage: 4%. I usually have this equal to the expense growth.

Cap rate change percentage: (-)0.10% annually. I never assume a cap rate compression.

3. Review Returns

After editing my scenario 2 analysis for items 1 and 2 above and freezing the purchase price at $700,000 (value from scenario 1), I will look at the primary metrics I care about with fixed assumptions for the various growth factors:

Year 1 Unlevered Yield On Cost (UYOC): 8.1% - not bad for a low effort value add plan (See this article for an explainer on UYOC)

Year 1 Cash-On-Cash Return: 10.9% - prettay prettay good

Year 1 Breakeven Occupancy: 67% - very good

10 Year Average Cash-on-Cash Return: 13.0% - very niiiiice

10 Year Levered IRR: 18.3% - I like it a lot.

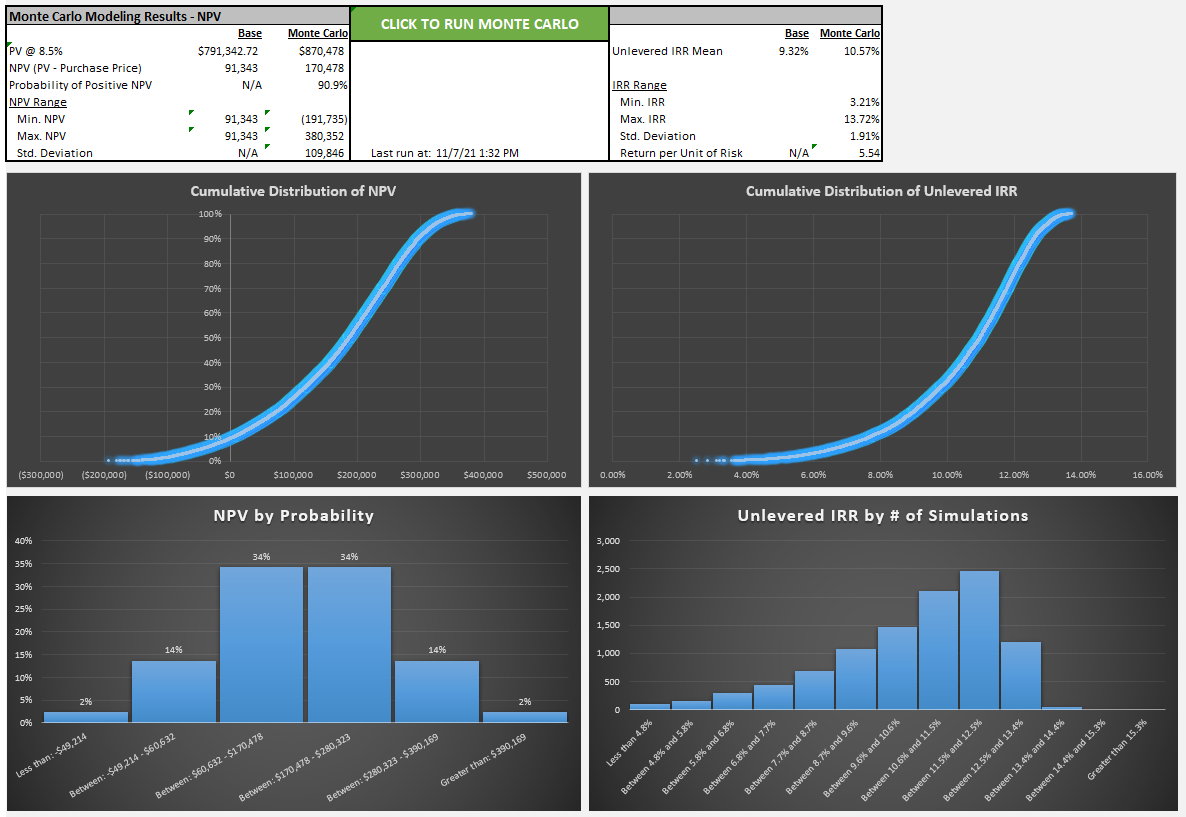

4. Run Random Simulation

The final step I do is determine my inputs for the Monte Carlo simulation. This simulation allows for me to enter ranges for all my growth assumptions and then runs 10,000 random simulations. The output looks like the following:

What this output tells me is that I have a decent likelihood of having higher returns than I predicted when using fixed numbers for growth assumptions. This improves my confidence in buying this property.

As a note, you can see that the Monte Carlo gives outcomes that have a negative net present value (NPV). This doesn’t mean there were outcomes where I lost money, it just means there are outcomes where I potentially overpaid (lower return than I had desired).

Final Thoughts

At a $700,000 purchase price, this property is a no brainer to buy. Given the current hot market, this property will likely sell for list price unless there’s something significant found during due diligence.

Would I break my rule and buy this for $749,000 even though in-place financials wouldn’t meet my scenario 1 8% cash-on-cash requirement? I think I would because the scenario 2 value add plan is very low risk in the current market of limited housing and huge demand for rental units. Finding 3 new residents to pay market rent will not be difficult if the current residents do not want to pay market rent.