Deal or No Deal: Valuing A 14 Unit Multi-Family

Deal or No Deal: Valuing A 14 Unit Multi-Family

Deal or No Deal: An ongoing regular series where I value a specific property. This property is a 14 unit apartment complex in rural Indiana.

In previous articles here and here, I showed you my 3 step process for evaluating a property:

Does this generally meet my screening criteria? Yes, go to 2.

Does this pass the sniff test a.k.a. back of the napkin math? Yes, go to 3.

Perform underwriting.

This will be my first article of an ongoing regular series where I use this process to evaluate a specific property. I will evaluate a range of property sizes from small to large, all within multi-family as that is the asset class I know best. And a lot of properties will be in the middle of nowhere as I like to invest in smaller markets to avoid the big real estate sharks. Typically larger properties require NDAs for the financial information, so most of my articles will focus on smaller properties, but the process to evaluate is exactly the same for larger properties.

The properties I evaluate in these articles will be listed online using publicly posted information that you can access yourself.

Spoiler alert: This one ended up being a total bust. Good job, good effort by me on picking a real beauty to start with.

Property: Pennville Manor Apartments

Source: Loopnet

Address: 250 E Main St, Pennville, IN

Units: 14

Asking Price: $570,000

Step 1: Does this generally meet my screening criteria?

Yes, so I will go to step 2. (Typically the properties I will evaluate for these articles don’t meet my personal criteria that I listed in this article, but maybe they will meet yours.)

Step 2: What is the back of the napkin math?

Information I need:

Unit breakdown

1 bedroom = 12

2 bedroom = 2

Market rents (Normally I already know market rents for an area, but for these random properties I am evaluating in areas I may not be familiar with, I will be using the fair market rents published by HUD, which are generally pretty accurate for middle of the road type properties.)

1 bedroom = $562/month

2 bedroom = $738/month

Market cap rate

8.5%

Napkin math:

Gross potential rent (GPR): ($562/month/unit x 12 units + $738/month/unit x 2 units) x 12 months = $92,722 annual GPR

Potential actual rent (6% vacancy/credit loss assumption): $92,772 x 94% = $87,159

Potential NOI:

30% expense ratio: $87,159 x 70% = $64,905

40% expense ratio: $87,159 x 60% = $55,633

Estimated value range

High: $64,905 NOI / 8.5% market cap rate = $763,590

Low: $55,633 NOI / 8.5% market cap rate = $654,505

Selling list price: $570,000

The list price is well below the low end of my value estimate range, so this is a potential good/great deal.

Since this property passes the napkin math test, I will proceed to full underwriting.

Step 3: Determine offer price based on full underwriting

If this was a deal I was actually pursuing, I would call the listing broker and possibly set up a property visit to assess the general condition. For the purposes of this article, I will use the online images and general assumptions of condition based on the age and property class.

The underwriting model I use is the Apartment Acquisition Model with Monte Carlo Simulation from A.CRE. I will estimate property value using two scenarios:

Property value with in-place financials

Property value with year 2 or so financials I believe are realistic

Scenario 1: Value with in-place financials

Determine adjusted NOI from in-place financials

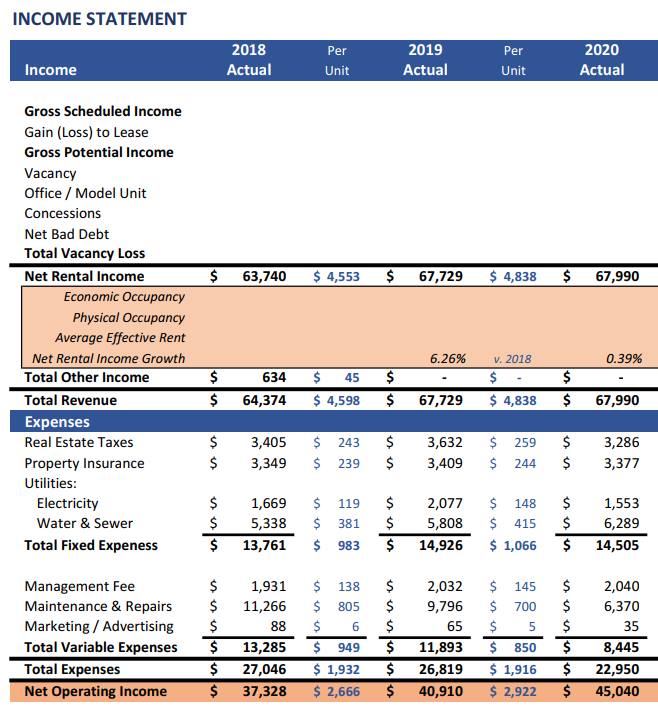

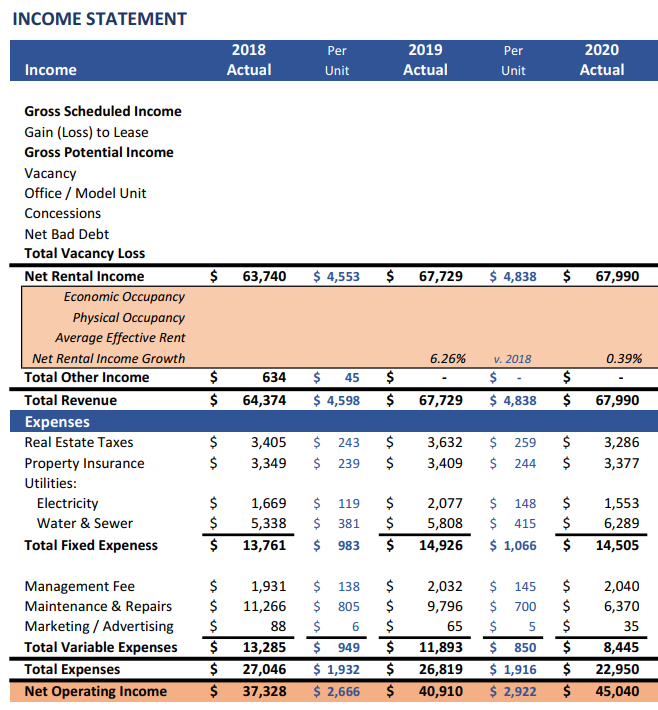

From the broker OM, below are the in-place financials. I will use the 2020 column to make my adjustments.

Property Tax: Per the assessor’s office, the current assessment is $159,200. If we were to buy at about $600,000, we can expect our tax to be about 4x the current, so I will assume $13,000 for annual taxes. This huge increase on the first item adjusted is already making me nervous that this property will not pencil out as feasible.

Normally you would want to call the tax assessor and find out specifically how properties are re-assessed at time of sale. I did not call the tax assessor to verify my 4x increase assumption as I would be wasting their time since I’m not interested in actually buying this property. Property tax increases can be a huge trap for a new buyer. Do your homework on what your assessed value will be in the future.

Property Insurance: Current property insurance is $241/unit. Based on my experience, this seems a bit low when including an umbrella policy. I will use $300/unit, so I will assume $4,200 for insurance. Normally you would want to receive a quote broke an insurance agent at this stage.

Utilities: I will use actual as listed.

Management Fee: Current fee is only 3% of revenue. This is very low for a property this small. My guess is the owners are paying themselves a small fee to manage themselves. I would normally expect a 3rd party management fee to be at least 6% for a small property.

Maintenance & Repairs: Current is 9.4% of revenue, which generally seems reasonable for a 1982 vintage property. I will assume about 10% to be conservative for $7,000 annually.

Marketing: Current of $35 may seem crazy low, but in the current rental market for properties like this that are in a rural area with minimal competition, there are many free advertising options that work just fine. I will use $100, but this will be inconsequential to the valuation.

Payroll: A small property like this requires no payroll. I will assume $0.

Administration: The in-place financials show $0 for this, but that is impossible. There are things like tax returns, bookkeeping, etc. that need to be accounted for in expenses. Even if you are doing these things yourself, your time isn’t free. I would assume $2,400 for this expense.

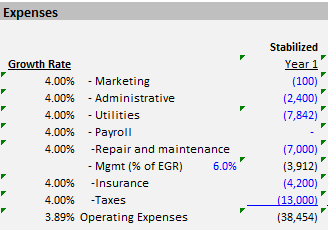

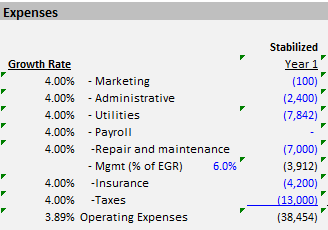

This is what my estimated year 1 operating expenses look like after making these adjustments:

Compared to the current owner’s in-place expenses, you can see I will have an additional 68% ($15,504) of annual operating expenses. This is an OpEx ratio of 56.5%, which is insanely high. Typical is 30-40%. Most of this huge increase is coming from the property tax increase. The current assessment being so low is a huge red flag and would be first on my list to track down with the tax assessor to make sure I am correct in assuming such a large increase.

Adjusted NOI = $65,198 revenue - $38,454 adjusted expenses = $26,744

Estimated value = $26,744 NOI / 8.5% market cap rate = $314,635

Obviously, I am not even close to the asking price of $570,000. Normally I would just stop here and go on my merry way. But for the purposes of going through the process for this article, I will continue.

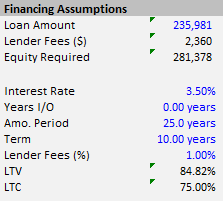

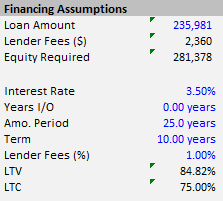

Determine Annual Debt Service

Using the below loan term assumptions, my annual debt service will be $14,177.

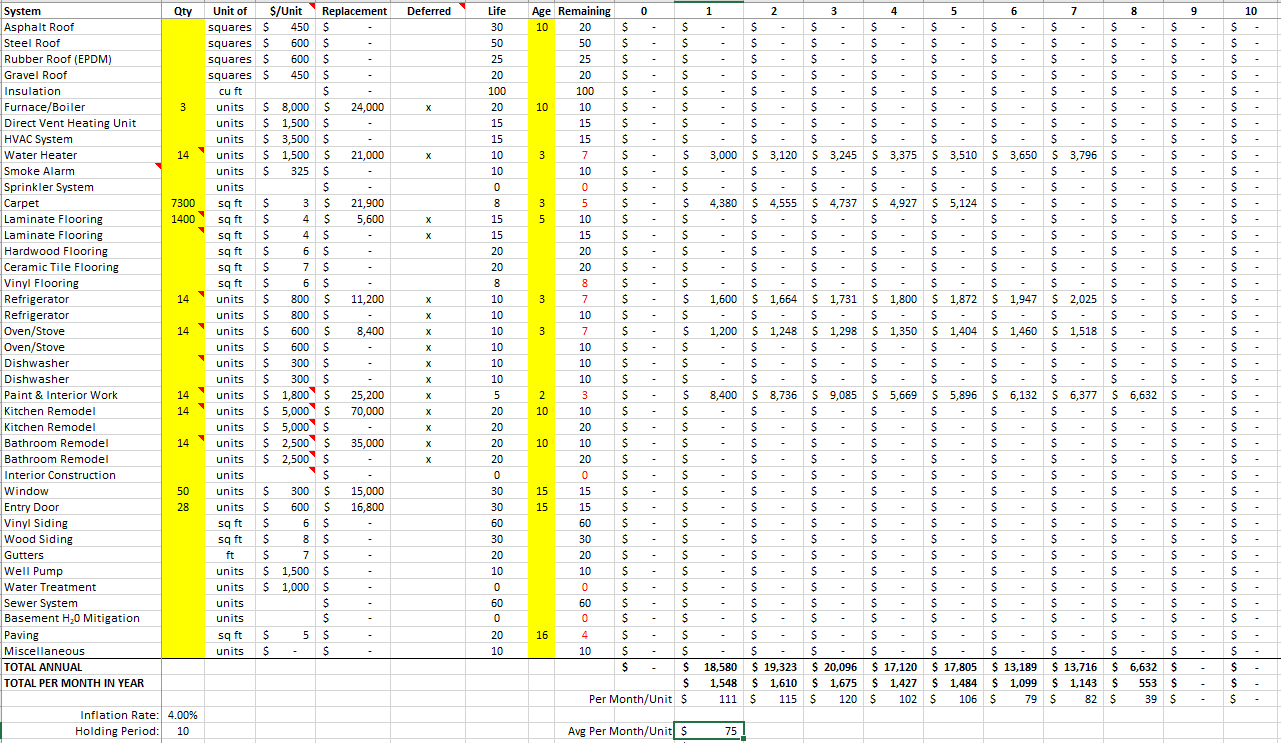

Determine Day 1 CapEx & Annual CapEx Spend

Day 1 CapEx

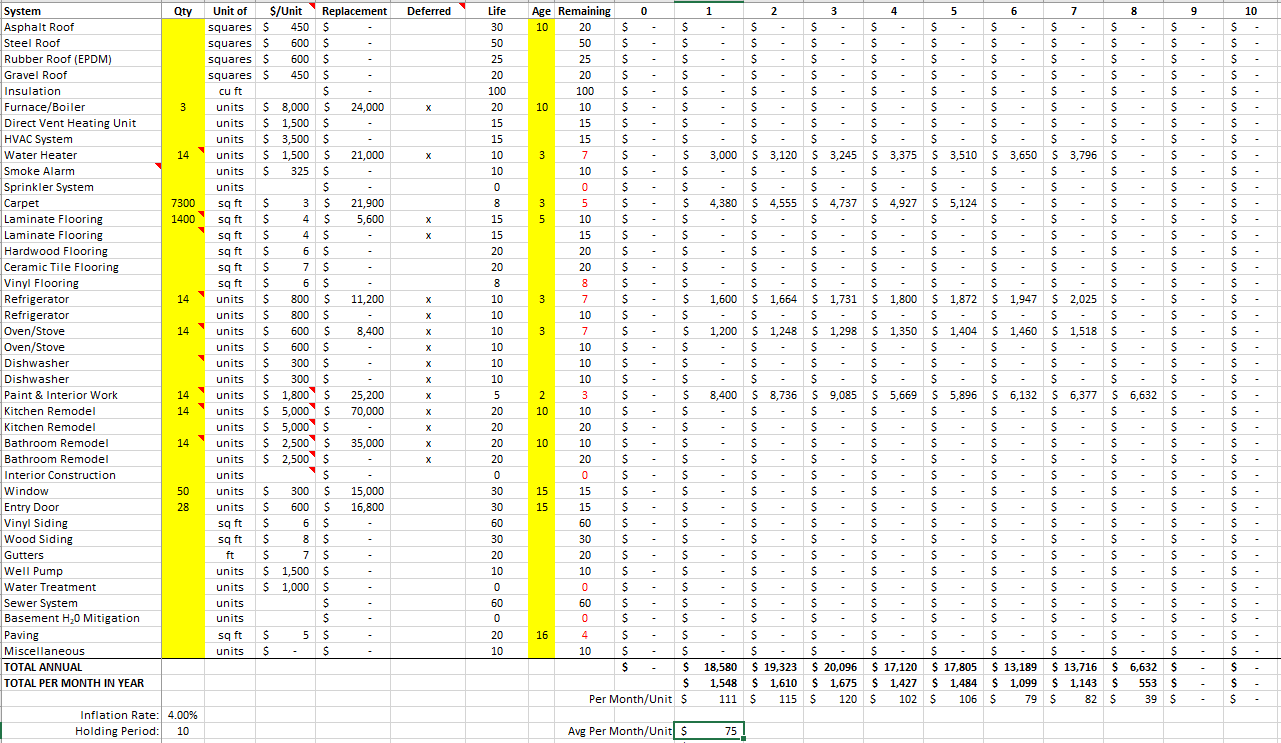

Reviewing the images in the offering memorandum (OM) and Google satellite and streetview, the property looks to be well maintained. The roofs appear to be in good shape, which are usually a huge potential capex expense. The OM states the roofs are 10 years old, which appears to be accurate.

The parking lot and sidewalks are cement. These appear to be in good shape per Google streetview. I will assume these have 80% life remaining.

The interiors are dated, but look in decent condition in the OM. Based on the overall condition of the property, I will assume that all units are in generally decent shape and have 70% life left for all interior capex items.

I can’t see any day 1 capex needed based on the images, but it will never be $0. I will assume I will need $10,000 to cover various day 1 capex.

Estimated Annual CapEx

I estimate annual capex spend with a spreadsheet that captures my entire holding period (10 years) and inflation estimate. If the remaining life of a capex item is longer than my hold period, I do not need to account for this item in my annual capex spend estimate - my spreadsheet will automatically put these as $0.

After filling in all the capex items based on my estimate of life remaining, it looks like this:

Because estimating capex is not a perfect science, I will take the average annual capex based on my hold period. For this property it is $75/month/unit, which is the unit of measure my model requires as an input.

This equates to $900/unit/year. The normal “rule of thumb” is to assume $250/unit/year for capex. You can see how off this assumption can be when you consider all possible capex over your hold period.

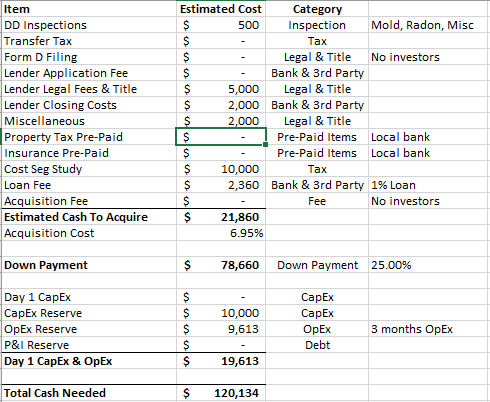

Determine total acquisition cost

My estimate for total acquisition cost is $120,134.

Determine year 1 cash-on cash return

Annual cash flow = Adjusted NOI - Annual Debt Service - Annual CapEx = $26,744 - $14,177 - $13,104 = (-)$536

Total acquisition cost = $120,134

Cash-on-cash return = (-)$536 / $120,134 = (-)0.45%

Obviously a negative cash-on-cash return is terrible. At this point, I will not even bother looking at scenario 2 of what value can be added as this will be a fool’s errand for me. Even though it appears there might be an opportunity to increase rents a good amount, I’m not interested in buying a property with negative cash flow on day 1.

Why Didn’t My Initial Screening Process Work?

Even with my initial screening showing it might be a great deal, it ended up being an absolutely atrocious deal. So where did my screening process fail?

Typically areas with very low market rents like this property, the 30-40% opex ratio assumption to provide a quick value may not work. The owner’s in-place opex was a reasonable 34%, so that checked out at my first glance. But my adjusted opex ratio jumped to 56.5% when I spent more time going through each expense line item. Typically two of your biggest opex costs are independent of the rent you can charge - insurance and tax. This makes the 30-40% opex ratio assumption fall apart in some instances like this when tax will increase by 4x.

It may be worth using a 40-50% opex ratio range for the quick valuation for low rent markets.

Final Thoughts

This valuation shows how critical it is to try to estimate a property value before spending time with full underwriting. I wasted about 30 minutes in total doing the full underwriting. This is a huge opportunity cost if you burn this much time on multiple properties a week. In the beginning as a newbie, there’s value in going through this process even if ends up being a waste of time. As you get more experience, it’s a cost of doing business so-to-speak, but make every effort to minimize going down a dead end road.

If you liked this article, please go to the nearest street corner and tell everyone that passes by to subscribe and to follow me on Twitter because there is no one else talking about real estate on the internet.